Can Australians buy property in Dubai? Yes. And the process is cleaner than buying an investment property in Sydney.

Most Australian investors I speak to assume there are restrictions, visa requirements, or a local partner involved. There are none. Over 60 designated freehold zones are fully open to you. No approvals. No complications. The confusion comes from outdated information, not the market itself.

Meanwhile, Sydney medians sit above AUD 1.3 million with rental yields stuck between 2.5% and 3%. Dubai recorded AED 138.7 billion in property transactions in Q1 2026 alone, up 21.2% year on year. The numbers are not subtle.

This guide covers everything you need to move forward. Ownership rights, exact costs, the full buying process, your ATO obligations, and how to secure a UAE mortgage as a non resident. By the end, you will know exactly where you stand.

What Legal Rights Do Australians Have to Own Dubai Property?

Full rights. That is the honest answer.

Dubai opened its real estate market to all foreign nationals through Law No. 7 of 2006 on Real Property Registration. Australian citizens are covered completely under that law. No nationality restrictions apply. There is no limit on how many properties you can hold. No local sponsor is needed at any stage.

As of 2026, the Dubai Land Department recognises more than 60 designated freehold zones where foreign buyers can purchase with complete ownership rights. These zones include the city’s most active and sought-after communities.

Freehold vs Leasehold: What Australians Need to Know

This is one of the first conversations I have with every new Australian client, because getting it wrong has real consequences.

Freehold means you own the property and the land it sits on. Full stop. You can sell it tomorrow, rent it out, renovate it, or pass it on to your children. There is no expiry. No conditions. This is the structure I recommend to almost every investor I work with.

Leasehold is a different arrangement entirely. You hold the right to use the property for a fixed period, most commonly up to 99 years. You do not own the land beneath it. When the lease expires, that right reverts to the freeholder. I rarely see experienced investors choose this route, and now you know why.

Always verify that the property you are considering sits within a designated freehold zone before you commit to anything. The DLD registry confirms this quickly.

Top Freehold Zones for Australian Investors

These are the communities I direct Australian buyers toward most consistently. They deliver on yield, hold value through cycles, and move well when you are ready to sell.

- Dubai Marina: Waterfront community with gross yields between 6% and 8%. Professionals and short-stay tenants keep demand strong year round. Resale liquidity here is excellent because there is always a buyer queue.

- Jumeirah Village Circle (JVC): This is my first recommendation for yield focused buyers. Returns are pushing past 7% in 2026. Entry prices sit well below Marina and Downtown, which means your capital goes further from day one.

- Business Bay: Central location, growing corporate tenant base, and a clear price appreciation trajectory. This area is moving upmarket, and buyers getting in now are ahead of that curve.

- Downtown Dubai: Premium entry price, but the Burj Khalifa address creates a value floor that nothing else in the city replicates. Capital growth here has been remarkably consistent over time.

- Dubai Hills Estate: Emaar built this one for families, and families keep choosing it. Parks, a golf course, and strong school access make it a retention play. Values hold well through slower markets.

Every freehold transaction is registered with the DLD. You receive a government-issued title deed. UAE federal law protects your ownership from the day the deal closes.

How the Buying Process Works from Australia

You never need to board a flight. I have guided Australian clients through complete purchases from Brisbane, Melbourne, and Perth without them setting foot in Dubai. The process is straightforward when you know the steps.

Step 1: Set Your Strategy and Budget

Do not open a property portal until you are clear on this. Are you buying for rental yield, long-term capital growth, or both? And what does your total budget look like once you include acquisition costs, not just the purchase price?

Here is a rough market map to orient you. Entry level apartments in emerging areas like JVC or Dubai South start around AUD 250,000 to AUD 300,000. One bedroom units in mid tier locations like Business Bay or Dubai Creek Harbour range from AUD 350,000 to AUD 500,000. Premium apartments in Marina or Downtown open at AUD 550,000 and go up from there.

One number worth keeping in mind: properties at AED 2 million, roughly AUD 830,000 at current exchange rates, qualify you for the UAE 10-year Golden Visa, which extends to your immediate family as well.

Step 2: Choose Your Developer and Project

Stick to developers with a delivery record you can actually verify. Emaar, DAMAC, Binghatti, Imtiaz, Ellington, and Omniyat all have completed projects listed in the DLD registry. If a developer cannot point you to finished buildings, that tells you everything you need to know.

Attending a Dubai Property Expo in your nearest Australian city is the most efficient way to compare multiple developers at once. Floor plans, payment structures, and direct conversations with project teams. Everything in one room.

Our Dubai Property Expo Australia 2026 guide covers the full event format. The Dubai Property Show 2026 guide breaks down what the investment seminars cover in detail.

Step 3: Sign the Agreement and Pay the Deposit

When you are ready to proceed, you sign a Sales and Purchase Agreement, commonly called the SPA. Deposits sit between 5% and 20%, depending on the developer and the specific project.

For off-plan purchases, your funds go into a RERA regulated escrow account. The developer cannot touch that money until independently verified construction milestones are reached. That protection is written into every off-plan transaction in Dubai, regardless of where the buyer is based.

Step 4: DLD Registration and Title Deed

The developer submits the transaction to the Dubai Land Department for registration. Your title deed is issued once that process completes. If you are handling everything remotely, a Power of Attorney lets a trusted representative in Dubai manage the paperwork on your behalf.

Ready property registrations typically take two to four weeks. Off plan registrations through the Oqood system are complete within 60 days of signing.

What Does It Actually Cost? The Full Breakdown

This section is where I spend the most time with first-time Dubai buyers, because the listing price and the total cost of acquisition are two different numbers. I want you to know both before you commit to anything.

Upfront Acquisition Costs

Plan for 7% to 10% on top of your purchase price to cover all closing costs in 2026. Those figures come from Property Finder and Dubai Land Department data. Here is exactly where that money goes.

- DLD transfer fee: 4% of the purchase price. The law technically divides this 2% buyer, 2% seller. In practice, buyers in Dubai carry the full 4% unless you specifically negotiate otherwise.

- Agent commission: 2% plus 5% VAT on resale properties when working with a buyer’s agent. Most off-plan developers cover this cost themselves.

- Trustee office fee: AED 4,200 for properties priced above AED 500,000. AED 2,100 for anything below that threshold.

- Title deed issuance: AED 580 for apartments and offices.

- Developer NOC fee: AED 500 to AED 5,000, depending on the developer. This fee is mandatory before any secondary market transfer can go ahead.

To put real numbers on it: a property at AED 1.5 million, around AUD 625,000, carries a DLD fee of AED 60,000 on its own. Once you stack everything else on top, you understand why I tell every client to budget total cost, not purchase price.

Critical 2026 note: transaction fees cannot be added to your mortgage. Every dirham of closing costs must be paid in cash at transfer. Check your liquidity before you reach that stage.

Ongoing Ownership Costs

Annual service charges fund communal maintenance, building security, landscaping, and general upkeep. Rates vary across communities and typically fall between AED 10 and AED 30 per square foot annually. On a 70 sqm apartment, expect to pay somewhere between AED 7,000 and AED 21,000 per year.

Beyond that: no annual property tax. No capital gains tax on sale. No tax on rental income at the UAE level. That combination is genuinely rare in any major property market.

Financing Options for Australians: Can You Get a Mortgage?

Yes, and the access is better than most Australians expect. UAE banks want international buyers in this market. Australian nationals sit on the approved borrower lists at Emirates NBD, HSBC UAE, Mashreq, and First Abu Dhabi Bank.

What Non-Resident Australians Should Expect

Non-resident terms differ from what UAE residents receive, so go in with realistic expectations.

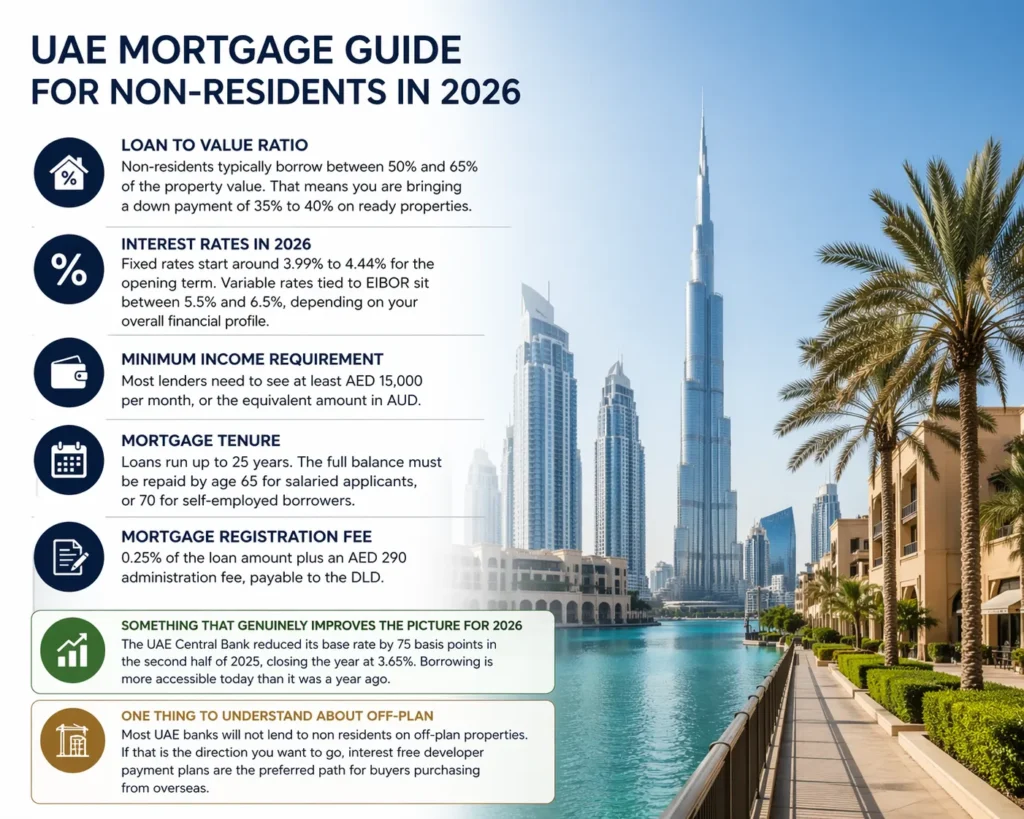

- Loan to Value ratio: Non-residents typically borrow between 50% and 65% of the property value. That means you are bringing a down payment of 35% to 40% on ready properties.

- Interest rates in 2026: Fixed rates start around 3.99% to 4.44% for the opening term. Variable rates tied to EIBOR sit between 5.5% and 6.5%, depending on your overall financial profile.

- Minimum income requirement: Most lenders need to see at least AED 15,000 per month, or the equivalent amount in AUD.

- Mortgage tenure: Loans run up to 25 years. The full balance must be repaid by age 65 for salaried applicants, or 70 for self-employed borrowers.

- Mortgage registration fee: 0.25% of the loan amount plus an AED 290 administration fee, payable to the DLD.

Something that genuinely improves the picture for 2026: the UAE Central Bank reduced its base rate by 75 basis points in the second half of 2025, closing the year at 3.65%. Borrowing is more accessible today than it was a year ago.

One thing to understand about off-plan: most UAE banks will not lend to non residents on off-plan properties. If that is the direction you want to go, interest free developer payment plans are the preferred path for buyers purchasing from overseas.

Tax Obligations: What the ATO Requires

Zero rental tax in Dubai. No capital gains tax when you sell. That is the headline, and it is a genuinely strong one. However, owning property overseas does not change what you owe the Australian government.

Your Reporting Duties Under Australian Law

Australian tax residents are required to declare income from every country, including Dubai. Your rental earnings go on your Australian tax return each year, and the ATO treats them exactly the same as income from a local investment property.

Here is what you need to keep on top of.

- Foreign property reporting: Any foreign asset valued above AUD 50,000 must be declared to the ATO. Dubai property clears that threshold easily.

- Rental income deductions: Management fees, maintenance, and depreciation are potentially claimable. Work with a tax advisor who has experience handling international property, not just domestic portfolios.

- No double taxation: Because Dubai charges no rental tax, there is no foreign tax offset to apply. You report the full gross income and pay Australian tax on it.

- Capital gains on sale: Any profit from selling your Dubai property is treated as a foreign capital gain in Australia. Own it for more than 12 months and the 50% CGT discount may be available to individual taxpayers.

What About SMSF Investors?

Australians can hold Dubai freehold property inside a Self Managed Super Fund. The investment needs to pass the sole purpose test, and your fund’s investment strategy must explicitly include overseas property.

Before you commit, sit down with your SMSF trustee and a financial advisor who understands the structure. The combination of zero UAE rental tax and strong gross yields makes the after-tax return genuinely attractive inside a compliant SMSF.

Why April 2026 Is a Different Kind of Opportunity

I want to be direct with you here, because this is not a generic market update.

Most of the articles you will find on buying Dubai property were written before the regional conflict. This one was not. I am writing it in April 2026 with full awareness of what happened and what has changed since.

Dubai property prices pulled back between 4% and 7% from their pre conflict peak. In the secondary market, sellers who held on through the uncertainty are now motivated. They are accepting terms that would not exist in a stable, rising environment. On top of that, the AUD has strengthened to around 0.69 to 0.70 against the USD since the ceasefire announcement, sitting near a three week high.

Lower Dubai prices. Stronger Australian dollar. Those two things do not line up very often. Together, they represent a dual entry advantage that simply was not on the table in January 2026.

The ceasefire came into effect on April 8, 2026. Talks are continuing. And every fundamental that made Dubai a compelling market before the conflict is still intact. UAE GDP growth is forecast at 5.0% for 2026, the fastest rate across GCC countries, according to FP Property research, citing IMF projections.

For a detailed breakdown of what the conflict meant for the market and how the recovery is taking shape, our Dubai property investment guide after the ceasefire covers everything you need.

Your Questions Are Answered. Now the Decision Is Yours.

The legal pathway is clear. Freehold ownership, zero annual property tax, yields that Sydney cannot touch, and mortgage access through major UAE banks. Australians have every right and every tool to buy in Dubai.

What I tell my clients right now is this. Prices are softer than they were three months ago. The Australian dollar is working in your favour. Developer payment terms are more flexible than they were at the start of the year. This is not a window that stays open indefinitely.

The Dubai Property Expo brings licensed developers, legal advisors, and investment consultants to Australian cities throughout 2026. Every exhibitor is DLD registered and vetted by Bright Realty International. Come with your questions. Leave with a plan you can actually act on.

Find your nearest event at dubaipropertyexpoaustralia.com.au.

Frequently Asked Questions

Here are some of the most frequently asked questions that actually hit when we thought about Can Australians buy property in Dubai?

Do Australians need UAE residency to buy property in Dubai?

No. Your Australian passport is sufficient. No UAE visa or residency permit is required at any point. Most of my Australian clients complete the entire process without leaving home.

What is the minimum investment for Australians in Dubai?

Off plan studios in areas like JVC or Dubai South start from around AUD 250,000, usually backed by interest-free developer payment plans. At AED 2 million or above, roughly AUD 830,000, you qualify for the UAE 10-year Golden Visa.

Do Australians pay tax on Dubai rental income?

Dubai charges zero rental tax. You still report that income to the ATO and pay Australian tax on it. Legitimate deductions can reduce your taxable amount. Get proper advice before your first rental payment lands.

Can Australians get a mortgage from a UAE bank?

Yes. Most major UAE lenders accept Australian applicants. Expect a 35% to 40% down payment at 50% to 65% LTV. Emirates NBD, HSBC UAE, and Mashreq all offer non resident mortgage programs.

How can Australians safely compare Dubai developers and projects?

Attend a Dubai Property Expo event in your nearest Australian city. You meet DLD registered developers directly, attend free investment seminars, and get tailored advice in a single sitting. Register at dubaipropertyexpoaustralia.com.au.